Automated Valuation Models

AVM’s and the Technology Myth

AVM Madness – How to Lose $50,000

AVMs

Misinformation about these so called “valuation products” is being bombarded on the public. The theme seems to be technology based and, in this race, they see the winner as the one with the most information. This campaign very well may be one of the all-time greatest sales jobs. And, at least for the moment, consumers are clicking right along, being sold on the idea that massive amounts of information (analyzed by a computer) is the answer to every valuation problem. AVM’s are being touted by many in the lending industry (among several others), as the best way to determine the value of your home. Do a quick search for “Home Values;” Google shows up about 150 Million sites that all have an opinion about your home’s value and real estate prices. Everybody is an expert, or so they say.

After over twelve years now of studying the AVM industry, the margin of errors is quite frankly, overwhelming. Sure, in the last five years they have improved. However, the very foundation by which they calculate home values is flawed, and since there is no other way for them to perform their calculation (without using public records), they level of quality information is as good as it can be; which is so low they should never be relied upon to determine a home’s value where a financial decision is to be made. For a general overview or for fun, they serve a great purpose. However, for determining the value of your largest lifetime investment, they are NOT the answer.

So let’s talk about this magic word; information. Pull up five automated valuation models and search for five properties. You’ll find one common denominator in every AVM; the square footage total listed by the local assessor’s office. I hate to state the obvious, but the “square footage fairy” doesn’t work for the tax department. He doesn’t work for the MLS, and slowly but surely the square footage information listed in MLS systems across the country is starting to resemble public records. Fear of “liability” seems to have replaced the listing agent’s due diligence or “responsibility” to homeowners (and their peers). If you review ten CMA’s, chances are, 90%+ will have the same square footage total listed in the local tax records. Somehow, the common knowledge that tax records frequently provide erroneous square footage details, seems to be overlooked and home values are being created (by agents and AVM’s) based on flat out wrong information. There’s that word again; information. What if the information they rely upon to determine home prices is wrong? At the end of this frenzy over automated valuation products, consumers may end up (once again) holding the short straw only to discover they have not paid (or received) a fair price for their homes. This current trend can only add insult to injury.

Is the square footage information listed in public records wrong enough to change home values? Remember the all powerful formula – price-per-square-foot? The answer to square footage errors in most cases is absolutely YES! In real estate valuation problems, short cuts don’t work. Real estate is a people business and will always require local knowledge. Somehow, this ever-growing problem seems to have escaped any national attention. The public has a right to know that AVM’s are great for fun and curiosity. However, when it’s time to tally up the family’s home value, call a real live person. Automated valuations (based on inaccurate square footage details) cost homeowners thousands every day. In the real estate industry’s “price-per-square-foot” world, these square footage errors are costing homeowners millions.

These information experts may be exposed as valuation imposters.

The AVM Fleecing of America

We’ve all heard about automated valuation models or AVM’s. You can find out the value of your home in a matter of seconds via any standard web browser. Home buyers (and sellers) now have access to more real estate information than ever before. And, since the beginning of the real estate crisis, the nation’s largest mortgage lenders have done a tremendous sales job trying to convince consumers that these computerized valuation services are just as accurate as traditional appraisers. Thanks to the changes brought about by the Home Valuation Code of Conduct (HVCC), people have become accustomed to seeing the words, AVM, BPO, and appraisal used interchangeably. Perhaps one of the goals of the HVCC, there has been a great push to convince the home buying public that these services are reliable. The FHA stated that they were pleased to see the improvement in the accuracy of their automated valuation products and made that decision based on comparing the numbers included in traditional appraisal reports against those provided by the computerized programs. They’ve done a great sales job and many people have followed just as they hoped they would. However, those that have had more contact and experience with these automated valuation services quickly learn just how dangerous they are. They are thousands of articles examining the stories of over and under stated values; wrong prices that caused consumers to lose a sale or not get a loan.

Where is Andy Rooney when we need him? Give me a break! This is a major fleecing of America, and it is growing every day. Without any national watchdogs keeping track of the numbers, the largest lending institution will have their way, dwindling down the numbers of qualified appraisers until eventually computerized valuation products will have to be used for mortgage lending. Take the appraiser out of the home buying process and it’s like giving the kids the key to the candy store.

The Perfect Business – Automated Valuation Models

Want to know the perfect business model? Sell information you get for free. It’s genius! What a deal. The tax department pays to collect and distribute property details and automated valuation models come along, put the information in a pretty package, and sell it back to the people who paid for it in the first place. Percentage-wise, the local tax assessor’s real estate values are more consistent than most AVM’s. And they have at least seen the property. The only information most AVM’s have is the details provided by the local assessor.

Take appraisers out of the mortgage process and lenders can find an AVM with the highest value to base their loan. Most AVM’s are known for over-estimating property values. And most do. If they listed conservative values consumers wouldn’t be flocking to these sites in the millions. Think about that. It’s brilliant. I just wish I had thought of it first. Home owners are desperate for any shred of good news concerning property values and along comes somebody to give them what they want.For the next few years, business will be great. Until statistical data is available that positively proves a margin of error, they will profit from providing often unrealistic property values. Over anxious consumers grasping at any good news about real estate values will continue to utilize these sites until they find out the truth.

Mark your calendars. Within the next ten years, AVM’s will be something listed in the history books as a result of the great financial climb and its ultimate collapse. They prospered during the good years and offered lenders a way to get loans approved without those pesky appraisers providing low values. After all, those pesky appraisers kept loans in check and it still went out of control. Where would we be now if not for the appraisers that held the line and kept even more mortgages from being approved based on over valuations. Every day some lender was trying to find a way to get their borrow a loan. Whatever it takes, we will get it done. Forget that the homebuyer can’t afford the house. That’s not important. We’ll let the next guy worry about that part. We just need to close the loan and get that commission.

We’re no where close to the end of the real estate crisis. Thousands of homeowners are still struggling one to month to get the mortgage paid. It’s just a matter of time before the ball falls again and a second round of foreclosures hits hard. It’s not a surprise decline. It’s just that no olne really wants to be the bearer of bad news. Facts are facts and the worst is yet to come. Get ready! The NAR is certainly not going to paint a negative picture. It’s their job to keep the news positive. They do the best they can with what they have to work with. All the seasonally adjusted and one of a hundred other terms thrown around, are designed just to deflect the actual numbers. The numbers are bad and any sugar coating does not change the facts.

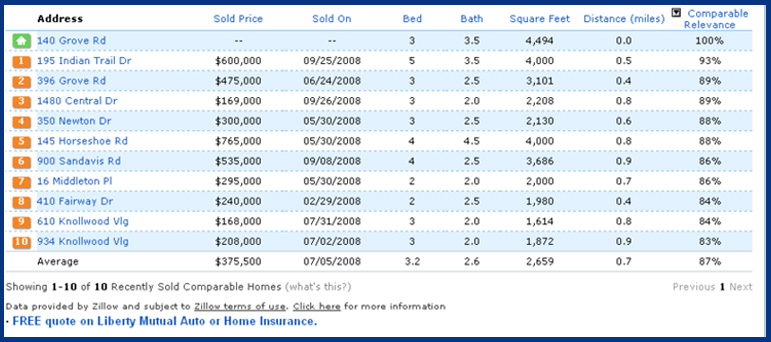

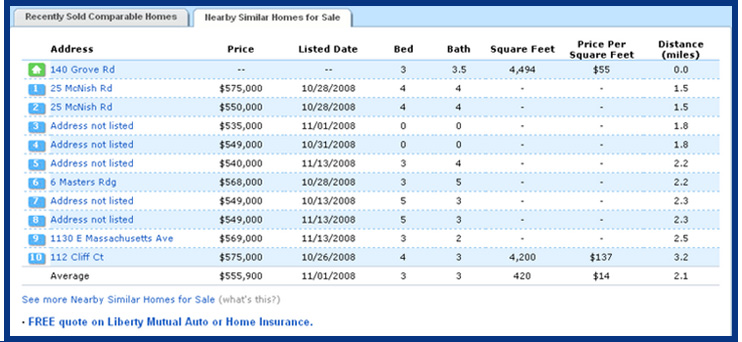

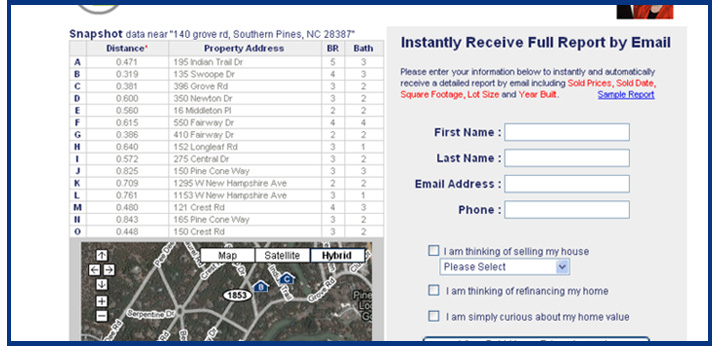

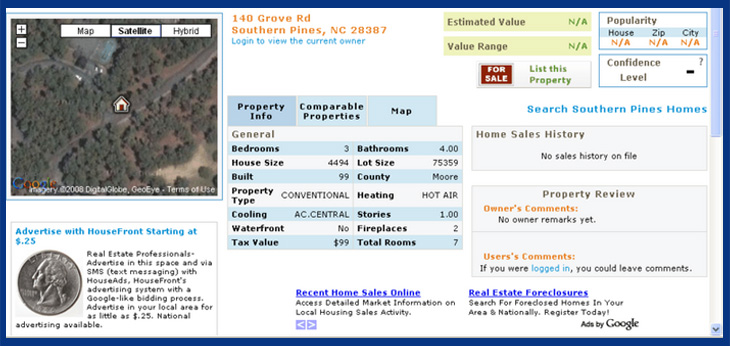

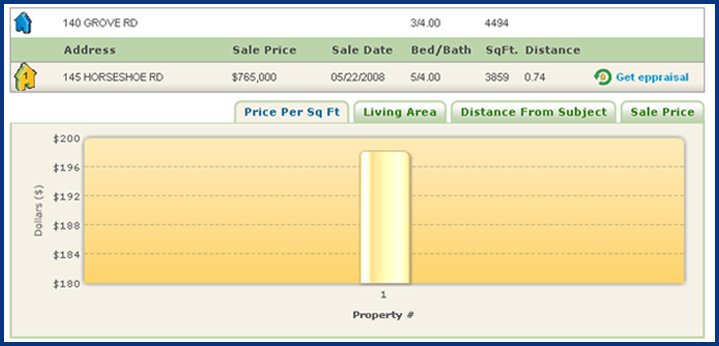

Let’s look at the property at 140 Grove Rd. and see how this works.

Zillow® – 140 Grove Rd. – 4,494 sqft

Yahoo® Real Estate – 140 Grove Rd. – 4,494 sqft

HomeValueHunt.com – 140 Grove Rd. – 4,494 sqft

House Front – 140 Grove Rd. – 4,494 sqft

EAppraisal – 140 Grove Rd. – 4,494 sqft

Start to see the pattern? Every automated valuation service shows this home with 4,494 square feet. The home actually has about 2,900 sqft with a partial finished basement. Even if you add the basement square footage to the upper level, the square footage total is over 600 sqft over the actual home dimensions. Do the math at $100.00 per-square-foot for a 2,900 sqft home and a 4,494 sqft home. Does size matter? If this house is used as a comparable sale, somebody is going to get shorted!

Just Say “NO” to AVM’s